Downstream front-end application layer will be one of the largest in the onchain economy

So many people calls for more applications but for the WRONG reasons – NO, it’s not about VCs trying to pump their infra bags NOR about finding the next 100x narrative to speculate on

Some thoughts – or ramblings really

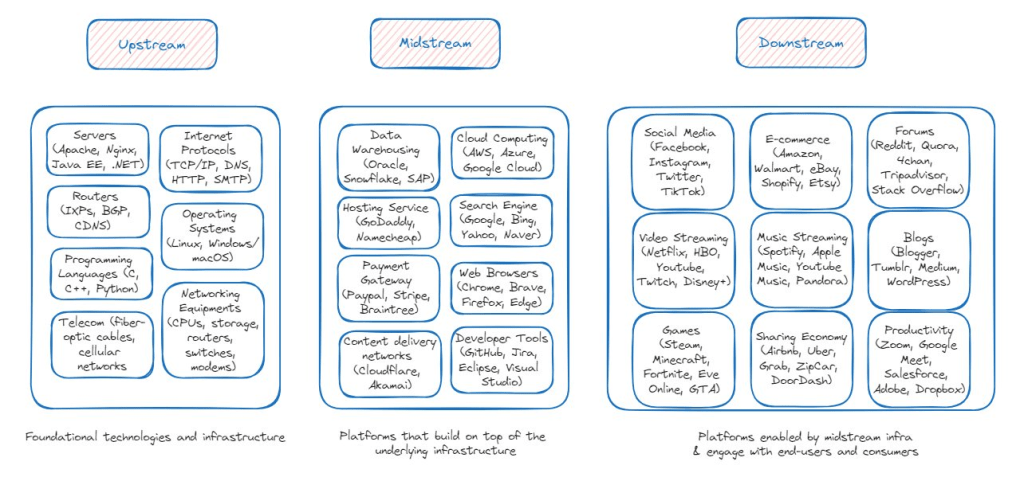

1/ Value Chain – Upstream, Midstream and Downstream

- To help understand how the crypto/blockchain space might eventually evolve, we could draw insights of how a matured industry like the internet is shaped up

- In the matured internet industry, its value chain could be dissected into upstream, midstream and downstream

- Upstream – foundational technologies and infrastructure that enable the internet; covering hardware, connectivity and networking, core software and protocols etc.

- Midstream – platforms that build on top of the underlying infrastructure; covering data storage, cloud computing, hosting services, search engine etc.

- Downstream – platforms that are enabled by midstream infra, and engage with end-users and consumers; covering applications like social media, streaming, e-commerce, blogs, forums etc.

- The upstream of the value chain often involves the development of the foundational technologies and encompasses development of core protocols and software that midstream platforms operate on. Midstream platforms acts as the crucial link – to ensure compatibility, optimization, and seamless integration between upstream infra and tech providers & downstream consumer-facing platforms. Downstream platforms serve as the primary interface and delivery channel to end-users where consumers will access and utilize products and services offered by these platforms.

- The infrastructure provided by upstream and midstream platforms enables downstream applications to provide a multifaceted product offerings and limitless iterations of such to address end-user needs

- Upstream and midstream infra typically has strong tech moats, homogeneous in nature with limited differentiation in product offerings, often being commoditized but still make steep profit margin (think Amazon AWS) thanks to strong tech moats, yet some has become public goods

- Downstream applications has low tech moats, but product offerings are differentiated with clear value proposition to attract users, focus heavily on retaining users and creating a strong network effect as the moat, many would horizontally expand to provide broader product offerings, some would even vertically integrate the whole value chain as they scale

- Upstream and midstream platforms – B2B

- Downstream applications – B2C

- As with the evolving blockchain/crypto industry, I expect the value chain will eventually shape up into the following 3 main streams:

- Upstream – foundational technologies and infrastructure that enable the adoption of blockchain; covering protocols & networks (L1/L2s), RPC/node infrastructure, execution & consensus clients, execution environment, consensus mechanisms, data storage, zkVM, DA etc.

- Midstream – platforms that build on top of the underlying blockchain infrastructure; covering economic security, AMMs, yield derivatives, intents/solvers, oracles, RaaS, staking & restaking, shared sequencers, interoperability, DIDs, lending markets, chain abstraction, data indexing etc.

- Downstream – applications enabled by upper stream infra; covering CEXes, DEX aggregators, orderbook DEXes, trading bots, games, Ce-DeFi, on/off-ramps, wallets, DePIN, social, gambling/betting, stablecoins

2/ Key observations/thoughts:

- Upstream crypto infra is becoming homogeneous. Infra projects are building on pretty much the same standardized mechanisms – e.g. PoS, EVM-compatible etc. The core services and capabilities are minimally differentiated. Despite there might be certain level of specializations or unique features some offer, the overall functionality provided by these upstream players are largely comparable.

- This homogenized nature of upstream products will eventually drive price competition as they strive to differentiate themselves on factors like pricing, performance, and builder-relationship management (for instance the commoditization of block-space). Creating a brand & network effect will be more important than ever for upstream players to stay relevant in the game.

- The phenomenon that upstream infra like L1/L2s doing most of the legwork of retail customer acquisition seems bizarre considering that their business models are very much B2B. Generically airdropping billions of dollars to users of multifaceted variations of downstream applications seems very inefficient. Imagine Amazon AWS spending billions of dollars to help its downstream clients like Robinhood for onboarding retail traders or Netflix for viewers – not knowing the intricacies of the products, user behavior/segmentation, engagement metrics etc. makes it hard to formulate the right incentive strategies for user onboarding & retention. Therefore, billions of dollars end up going down the drain to onboard airdrop farmers and mercenary users that will churn once incentives are over.

- Midstream crypto infra is likely to face the same fate of becoming homogenized and eventually commoditized. For DeFi “apps” like Uniswap, Aave and Pendle – I intentionally categorize them as midstream given the limited differentiation between players of the same subsector and for the fact that they will need intuitive downstream applications (e.g. frontend aggregators/CeDeFi platforms) with better UX/UI to facilitate usage and scale. The current user experience they offer tend to cater only to crypto-natives (let’s be real: setting up and funding a hot wallet, navigating to the DeFi app, choosing the right product/trading pairs, picking the right chains, confirming the tx etc. is a real pain in the ass for most non-native users).

- Many of the midstream infra are still at the iterative stages (especially intent layers/solver networks, coprocessors, shared sequencing, chain abstraction) – as the technologies mature this segment will enable better functionality of downstream applications – faster/ cheaper/more precise execution and computation, better interoperability, smoother user experience…

- Downstream crypto applications segment is FAR from reaching a matured state. Would expect the scale of downstream segment to outweigh the upper stream segments – akin to the market structure we see in matured industries.

- Two main categories of downstream applications – Centralized & Decentralized. Centralized applications (CEXes, CeDeFi platforms, on/off-ramp services) offers a more intuitive UI/UX which is quite familiar with Web2 platforms with minimal onboarding friction, typically regulatory compliant, and most have already found some sort of product-market-fit. Decentralized applications leverage & aggregate the upper streams infra as their backbone while providing frontend interfaces with a smoother user experience that reduce user friction. This segment will be at the forefront of accelerating mass adoption of blockchain technologies & crypto.

- Vertical integration – seeing a trend where downstream applications that have already found PMF begin vertically integrating across the whole value chain and horizontally expanding to offer a broader scope of services. A phenomenon that is not unheard of – Amazon online bookstore (downstream) built its own logistic/fulfillment network (midstream) and cloud-based infrastructure (upstream) to power its e-commerce and other internal operations & horizontally expanded its e-commerce offerings into every retail category. In crypto – consider CEXes like Binance & Coinbase (downstream) launching BNB Chain & Base (upstream), incentivizing the integration and building of midstream infra on top, and horizontally expand to offer a broader range of products – wallets, staking services, on/off-ramps, custodian etc.; or consider the game Axie Infinity (downstream) launching Ronin Chain (upstream), and all the midstream apps/infra – Ronin Wallet, Katana (DEX), Mavis Market (NFT Marketplace), Ronin launch pad, Mavis ID (DID), Ronin RPC etc.

- I expect the customer acquisition heavy-lifting will shift from upstream infra back to downstream applications. This would be catalyzed by 1) L1/L2 ecosystems direct airdrops to applications giving them discretions on designing incentive programs according to their respective roadmaps, product designs and business models 2) VCs, L1/L2s and retail capital re-rate downstream applications, funding the growth of such segment

3/ Applications in the mid/down-stream of the value chain will accrue the most value

- On value creation – Upstream infra creates value by pioneering technological innovation, improving performance, efficiency, and reliability of the underlying systems. Midstream platforms create value by packaging the upstream tech offerings into builder-friendly applications, platforms or ecosystems that tackle specific market needs. Downstream players create value by enhancing the usability, accessibility, and personalization of their product offerings, by leveraging on the midstream & upstream infra.

- Current state – Upstream/midstream infra has gone through 2-3 cycles of technological iteration. A lot of the value created from the tech advancement has been reflected in the growth of market capitalization of the sectors. Innovation has gone plateau, technology homogenized. Downstream applications on the other hand, are prone to experience unparalleled growth as they begin to create value by leveraging the maturing upper stream infra in this/upcoming cycles.

- In a matured industry, downstream platforms/ applications often gain the most mindshare as they are essentially the only interfaces users interact with. Users wouldn’t even know (nor care) the backend stacks these downstream applications build on. What the users care the most is the user experience these applications bring.

- With a strong network effect (user-base) and differentiated product offering, downstream platforms are enable to command a higher pricing power and be valued at a higher valuation

- Consider ByteDance (parent co. of TikTok) with 50m+ DAUs generating $120bn revenue valued at $268bn vs Akamai (CDN network that they build on) generating $3.8bn trading at $16bn in 2023; the same applies to Meta, Netflix, Google and so on

- Value flows from downstream applications that monetize on a huge network of paying customers, to midstream and eventually upstream participants. There’s this symbiotic relationship where the growth of downstream apps will eventually fuel the growth of the underlying upstream technologies they rely on.

- We already see crypto applications accruing more fees than upstream infra – midstream (Raydium, Uniswap, PancakeSwap, Aave, Lido, Jito) ; downstream (Ethena, Pump). Upstream infra like Avalanche, Near, Polygon and a long list of alt L1/L2s are already out of the picture generating merely 10-100k of fees a day.

- Simply consider the case of say Uniswap vs Ethereum: a user trades $100,000 on Uniswap, pays $1 network transaction fees to Ethereum, but Uniswap banks $300+ from exchange fees + MEV profits – it’s pretty clear which layer accrues more value

4/ Proliferation of profitability maximization

- Downstream applications on L1/L2s are on one hand taxed gas fees (L1 security fees and/or L2 execution fees) for user activities while also having MEVs exploited by block builders of upstream L1/L2s, leaving a lot of money on the table.

- Intuitively, to maximize revenue streams, many downstream apps begin exploring the possibility of taking back the sovereignty of revenue generation

- Expect downstream applications to further privatize its own order-flow by vertically integrating to construct its own private mempools or even becoming a block builder. Some might even launch its own app-chain as a mean to capture more value.

- Consider frontends like the Banana Gun TG bot – on track to paying over $100 million to Ethereum builders and validators in priority fees and miner tips. Already has 98% of the orderflow goes through private mempools. Wouldn’t be surprised if Banana Gun expand vertically to run block-building to capture even more value.

- Some opt for building its own appchain for a more optimized blockchain architecture specific to the app (throughput requirement, consensus algorithms, app-specific data structures, custom gas fees and economic incentives, sovereignty etc.), enabling it to scale more effectively than general-purpose blockchains. Value capturing will also concentrate on the appchain instead of doing “rev-share” with the base layer blockchain.

- Expect to see profitability of applications to grow as infra like solver networks (Fastlane Atlas, Semantic Layer, Uniswap V4 hooks), interoperability & chain abstraction infra , as well as RaaS & rollup stacks (OP stack, ZK stack, Arbitrum Orbit etc.) to mature and popularized, allowing for better value capture down the road

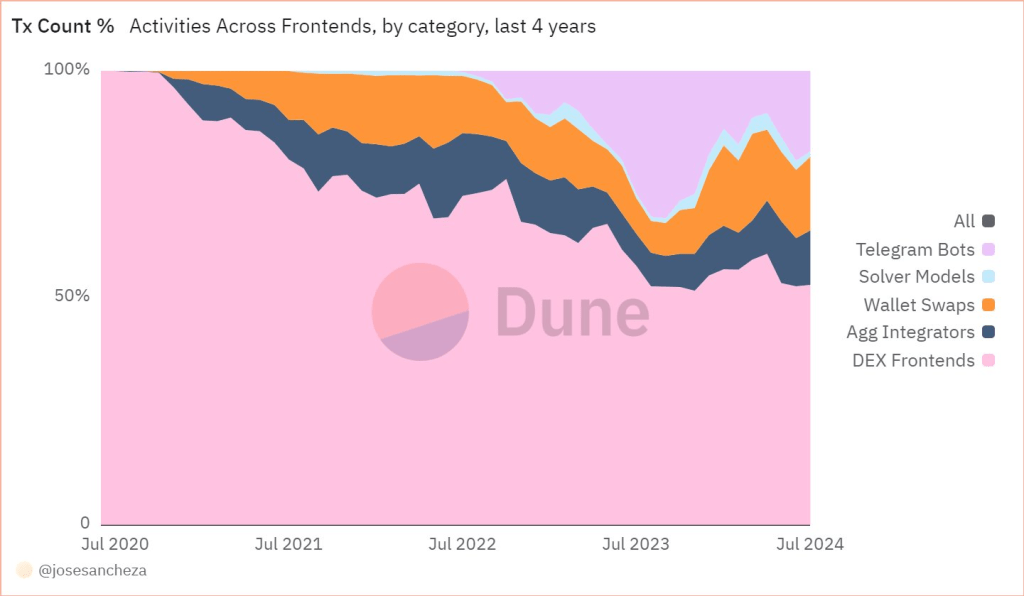

5/ The “Frontends Flippening” meta

- Downstream frontend applications that offer streamlined user experience will be at the forefront of onboarding millions of non-cryptonative users. Midstream applications like Curve, Aave, and upstream infra will instead become the backbone for execution and settlement

- Frontend applications I’m especially bullish about: Trading bots/ Wallet in-app swaps that provide chain-abstracted trading experience with optimized trades execution and low fees; Orderbook/CLOBs that offer a Web2-like trading experience with fast & cheaper execution; Payment superapps that come with on/offramp solutions + seamless P2P Venmo-like experience for stablecoin transfer; Social apps & Games that sensibly leverage financialization + asset ownership + AI to create experiences that would rival Web2 apps

- “Frontends Flippening” is happening

- Consider downstream frontends like Jupiter and 1inch collecting the similar level of fees as Uniswap and PancakeSwap

- Or consider frontends like TG bots + wallet swaps + aggregators already generating approx. 50% of all transactions on Ethereum

- Downstream frontends are eating up the market share of midstream backend applications. As these frontends become the de facto standard for interacting with DeFi, expect the market share of backend apps to further decline.

The flippening of frontend fat apps is inevitable.